Economics 101: Credit & Debt Cycles.

Although the United States economy is a huge behemoth of a “machine”, there are four fundamental forces that you really need to understand in order to figure out how the US economy (or, for that matter, how any economy works).

The short term debt cycle, long term debt cycle, deleveraging, and productivity

I) So what makes up the economy?

It’s the sum of all the transactions that happen amongst players. Think of players as people, companies etc. The simplest form of a transaction is between a buyer and seller.

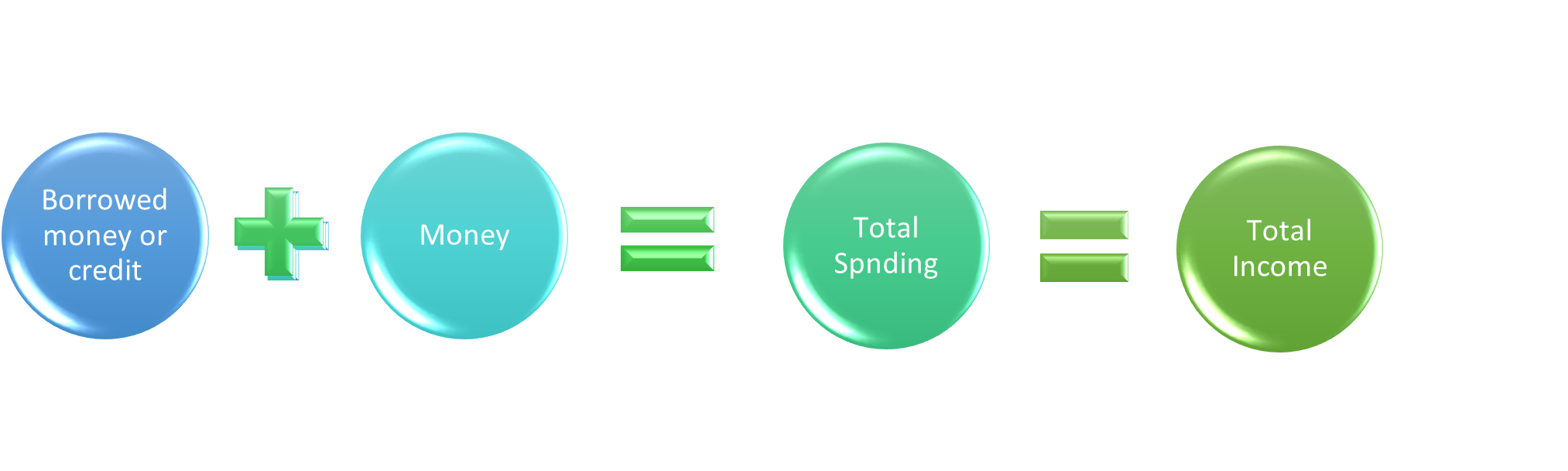

Fundamentally, and at its roots, a transaction occurs when Player A uses its money or borrows (credit/debt) money in order to buy something from Player B (goods, services, or assets). The sum of the amount of money or borrower money is the total spending in the economy. Since every dollar of spending that Player A does is earned (or income) to Player B, total spending in an economy is also the total income in the economy.

To summarize:

A market consists of the sum total of all transactions between all the buyers and sellers of the same good, service, or financial asset. There are many markets (think market for food, automobiles, electronics, real estate, stock market etc.) The economy is the sum of all these markets and the transactions that occur within those markets.

II) Credit

Credit is an extremely important concept. Believe it or not, there is way fewer actual money circulating in the economy than there is money that is being borrowed ($226 trillion+ globally as of 2020). Credit is debt: your mortgage, student loan, automobile loan. Credit is created when a lender gives someone or something money with the expectation that the money will be returned with some additional interest. When credit is created, it becomes debt. Debt is a liability to the person or thing borrowing, but it is an asset to the lender. Credit is so important because as we see from the equation above, when someone borrows money and then spends it via a transaction with someone else, there is more income earned, which drives the economy, creating economic growth.

III) Short term credit/debt cycle:

In the short term, economic swings are driven by debt (every few years (5-10 years) These are economic booms and recessions. In the short term, income can be driven by borrowing. In a “boom” or expansion, as more and more borrowing happens in the economy, spending and incomes go up. Over time, the amount of spending and income outpaces the amount of increase in goods, services, and assets in the economy. This causes prices to rise as demand for those goods, services, and assets outpaces the supply, so people bid up prices for them, because of the principle of scarcity (the less there is and more competition for a good, the more “valuable” or pricey it is to have). This increase or growth in prices is inflation.

There is always a natural “healthy” or long-term inflation or increase in prices in an economy. The American Central Bank or the Federal Reserve usually targets 2.0% price growth every year. However, high inflation (as we have right now in the global economy) is a bad thing: it reduces your ability to purchase things, and we all become poorer and lose our savings, and generally all are able to afford less goods and services as a result. Runaway inflation or hyperinflation in countries such as Zimbabwe or Venezuela results in terrible standards of living and all around social and economic unrest and hardship for those countries’ citizens. So, over-time, to prevent inflation from becoming hyperinflation, the Federal Reserve, and other central banks around the world increase interest rates (which is the cost of borrowing). Remember, borrowing or credit drives economic growth by increasing spending and income. However, if the cost to borrow or the cost of getting credit is increased, then less borrowing will happen, and accordingly less spending and income. This, in turn, will result in less spending or less demand for goods and services, which will combat inflation.

As interest rates go up to fight inflation, there is less spending, and therefore the economy starts to contract, going from a “boom” not to a “contraction” or a “recession” with two consecutive quarters of negative GDP growth.

That is the short-term debt cycle. Eventually, as price growth slows down, the Federal Reserve will decrease rates to increase spending again.

IV) Long-term debt cycle & Productivity

Over the longer term, as these short-term debt cycles happen over and over again, the amount of debt in the economy slowly continues to trickle up. This coincides with the idea that over-time incomes generally go up as productivity increases; as incomes go up over the long-term, so does the amount of borrowing in the economy, and so does the amount of debt. Think about how people’s standards of living have gone up over the years due to technological innovation:

A middle-class Average Joe today enjoys a standard of living much better than the wealthy business magnate and tycoon John Rockefeller did in the 19th and early 20th century, due largely to technological progress.

As a result, debt is growing long-term at a rate higher than incomes are growing. This is the long-term debt bubble. Eventually, this is unsustainable, and this process reverses as people can no longer pay their debts. This causes the bubble to pop, resulting in the deleveraging process. During this process, people stop spending rapidly and also stop wanting to borrow. Incomes fall. Credit dries up. Borrowers sell assets to service debts. This rush to sell those assets cause asset prices to fall off a cliff. Banks experience runs. The stock market tanks. Real estate prices plunge. This severe contraction is a depression. In times like this, social and political unrest are likely to emerge. The difference between deleveraging and a recession is that interest rates are so low, eventually hitting 0%, and they cannot be lowered anymore to create economic growth and reverse this pessimism. In the United States, this happened in the 1930s and once again in 2008. This long-term debt cycle between deleveraging period tends to occur every 75-100 years.

How do we get out of a deleveraging? Ultimately, debt burden needs to come down. There are four things that happen: (1) wealth transfer from the wealthy to the poor, (2) spending is cut dramatically (or austerity), (3) debts reduced via lenders accepting less or writing off parts of the debt, (4) the central bank prints money to stimulate growth. In every deleveraging in the history, all four of these things have happened in order to get the economy out of a deleveraging period. Over-time, these strategies start creating income growth again and less debt, resulting in growth, and another boom period, starting the cycle all over again.

inspiration from Ray Dalio.